Self Directed IRA (Individual Retirement Account)

A self-directed IRA (SDIRA) is a type of Individual Retirement Account (IRA) that allows you to invest in a wider range of assets beyond traditional stocks, bonds, and mutual funds, including real estate, precious metals, and private placements. (Please consult with your Tax, Accounting or financial planning professional)

Here's a more detailed explanation:

Key Features of a Self-Directed IRA:

Flexibility:

SDIRAs offer more flexibility in investment choices compared to regular IRAs, allowing you to invest in alternative assets.

Alternative Investments:

You can invest in assets like real estate, precious metals, private equity, cryptocurrency, and more.

Self-Managed:

While a custodian or trustee manages the account, you, as the account holder, are responsible for making investment decisions and managing the assets.

Tax Advantages:

SDIRAs retain the same tax advantages as traditional or Roth IRAs, meaning contributions may be tax-deductible (traditional IRA) or withdrawals are tax-free (Roth IRA).

Specialized Custodians:

SDIRAs are typically available through specialized firms that offer SDIRA custody services.

Important Considerations:

Due Diligence:

As you are responsible for managing the investments, thorough research and due diligence are crucial.

Rules and Regulations:

SDIRAs are subject to IRS rules and regulations, including those related to prohibited transactions (e.g., "no self-dealing" rule).

Potential Risks:

Investing in alternative assets can involve higher risks, such as illiquidity and potential fraud, so it's essential to understand the risks involved.

Seek Professional Advice:

Consider consulting with a financial advisor and tax professional to understand the implications of investing in a self-directed IRA.

Self Directed 401K Retirement Plan

A self-directed 401(k) is a retirement plan that allows you to invest your retirement funds in a wider range of assets, including real estate, private equity, and precious metals, rather than being limited to traditional investments like stocks and bonds. Here's a more detailed explanation: (Please consult with your Tax, Accounting or financial planning professional)

• Increased Investment Options:

Unlike traditional 401(k)s, which typically offer a limited selection of mutual funds and stocks, a self-directed 401(k) allows you to invest in a wider array of assets.

• Greater Control:

You have more control over your investment choices and can tailor your portfolio to your specific needs and risk tolerance.

• Tax Advantages:

Self-directed 401(k)s offer the same tax advantages as traditional 401(k)s, including tax-deferred growth and potentially tax-free withdrawals in retirement (depending on the type of 401(k) - Roth or Traditional).

• Suitable for Self-Employed Individuals:

Self-directed 401(k)s, also known as solo 401(k)s or individual 401(k)s, are particularly well-suited for self-employed individuals and small business owners who want to save aggressively for retirement.

• Contribution Options:

You can make contributions as an employee and as an employer, potentially doubling your contribution limits compared to traditional retirement accounts.

• Rollover and Withdrawal Rules:

The withdrawal and rollover rules are the same as for traditional 401(k) plans or IRAs.

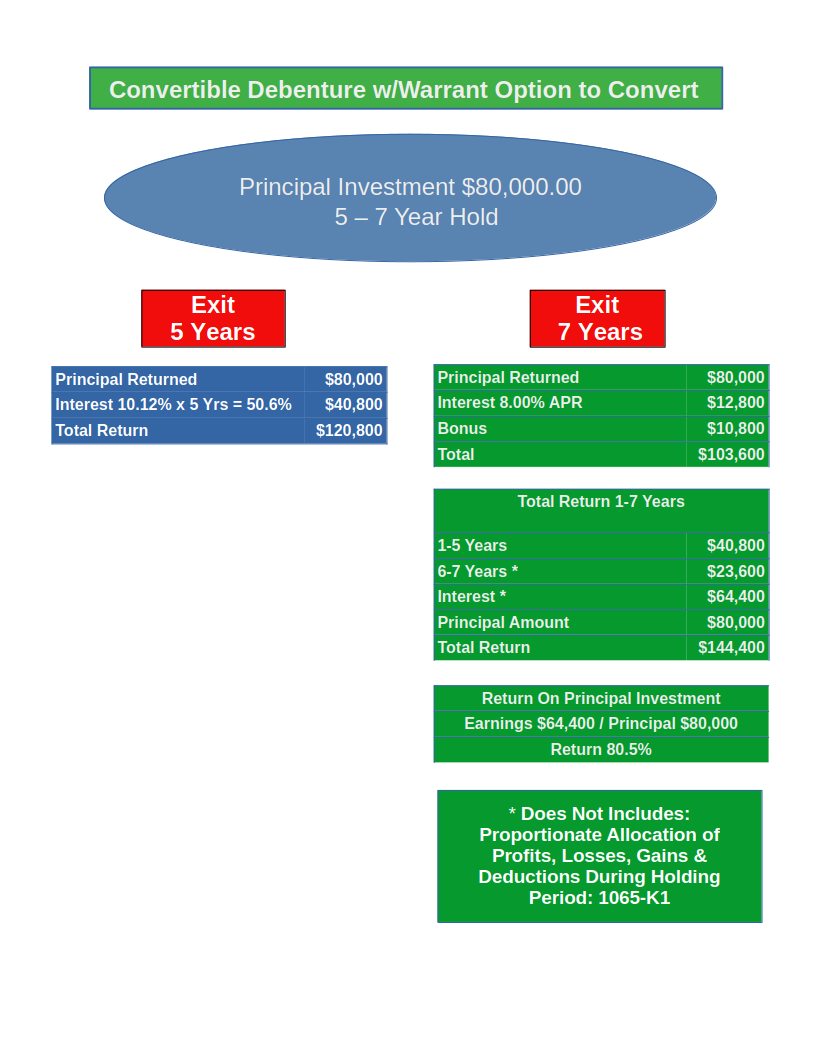

Examples of Investments:

• Real estate

• Private equity

• Precious metals (gold, silver, etc.)

• Digital assets (cryptocurrencies)

• Syndications

• Hedge funds

• Promissory notes

• Tax liens

• Mortgage notes